📌 Table of Contents ⬆

Best High-Yield Savings Accounts 2026: Earn 5%+ APY Today

If your money is sitting in a traditional bank savings account earning 0.01% APY, you're leaving hundreds — possibly thousands — of dollars on the table every single year. In 2026, the best high yield savings account options are offering rates above 5% APY, a dramatic shift driven by the Federal Reserve's aggressive rate-hiking cycle that began in 2022. With inflation still a factor in everyday budgets, maximizing every dollar of interest income has never been more critical for American savers.

For more information, see: Bankrate: HYSA Rates, NerdWallet: Best Savings Accounts

📌 Quick Summary

- High-Yield Savings Accounts (HYSAs) outperform: The best accounts in 2026 offer over 10x the national average APY, meaning a $10,000 deposit earns ~$525 annually vs. ~$45 at a traditional bank.

- FDIC insurance protects your money: Every account on our list is FDIC-insured up to $250,000, so there is zero risk to your principal while you earn competitive returns.

- Online banks dominate the top rates: Because they carry lower overhead than brick-and-mortar banks, online institutions consistently pass savings on to customers through higher interest rates and fewer fees.

📊 Best High-Yield Savings Accounts 2026: Top Rates Compared

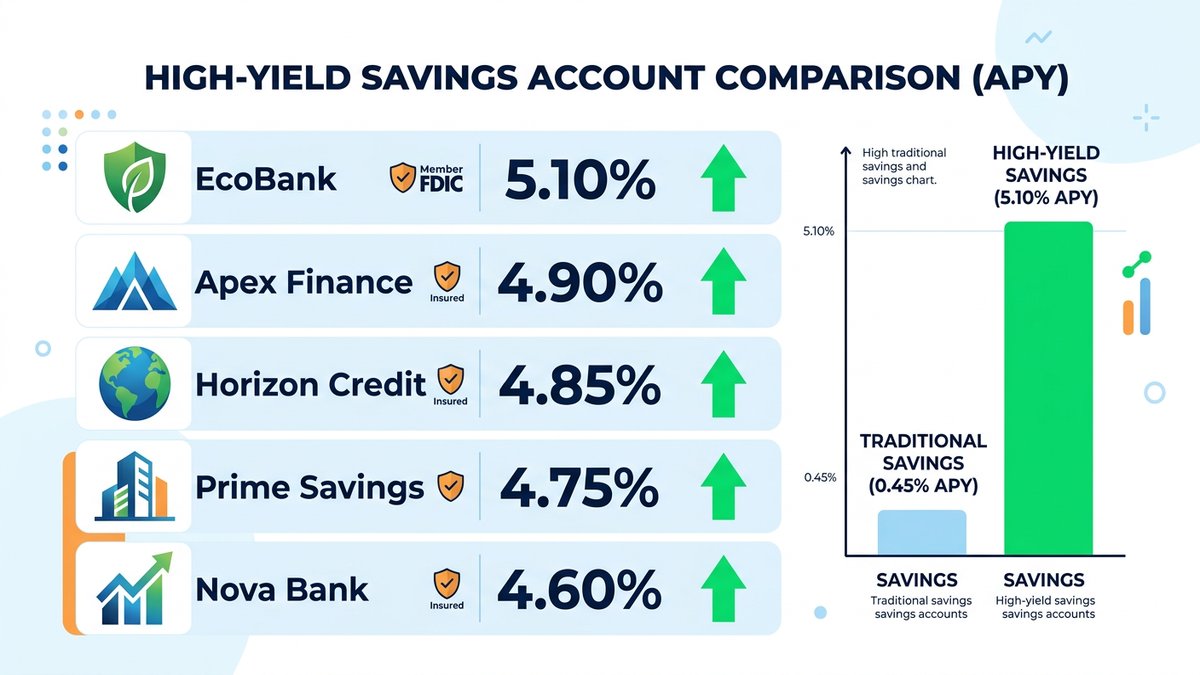

Finding the best high yield savings account in 2026 requires looking beyond the headline APY number. You need to evaluate minimum balance requirements, monthly fees, ease of fund access, mobile app quality, and whether the institution is FDIC-insured. The good news is that competition among online banks has intensified significantly, which means consumers are benefiting from the most favorable savings rate environment seen in over two decades. According to the FDIC's national deposit rate data, the average savings account APY sits around 0.45% as of late 2024, while top-tier high-yield accounts are consistently posting rates between 4.75% and 5.25%. That gap represents a massive opportunity cost for anyone who hasn't yet made the switch. On a $25,000 balance, the difference between 0.45% and 5.10% APY amounts to roughly $1,162 in extra interest income per year — money that could fund a vacation, bolster your emergency fund, or accelerate debt payoff goals.

The landscape of high-yield savings in 2026 is dominated by online-only banks and fintech platforms, which have a structural cost advantage over traditional branch-based banks. Without the expense of physical locations, ATMs, and large in-person staff, these institutions can allocate more revenue toward competitive interest rates and customer-friendly features. Banks like SoFi, Marcus by Goldman Sachs, Ally, Discover, and American Express National Bank have consistently ranked among the top performers year after year, and 2026 is no exception. Many also offer perks like no monthly maintenance fees, no minimum balance requirements, and same-day or next-day fund transfers to linked checking accounts. It's worth noting that APYs are variable and can change with Federal Reserve policy shifts, so staying informed and periodically comparing rates is a smart habit for any disciplined saver. The table below captures a snapshot of the top accounts available right now, so you can make an apples-to-apples comparison before choosing where to park your hard-earned dollars.

SoFi High-Yield Savings

Up to 5.10% APY with direct deposit setup

Marcus by Goldman Sachs

4.90% APY, no fees, no minimums required

Ally Bank Online Savings

4.85% APY with buckets & round-up savings

| Bank / Institution | APY (2026 Est.) | Min. Balance | Monthly Fee | FDIC Insured |

|---|---|---|---|---|

| SoFi High-Yield Savings | 5.10% | $0 | $0 | Yes (up to $2M via partners) |

| Marcus by Goldman Sachs | 4.90% | $0 | $0 | Yes ($250K) |

| Ally Bank Online Savings | 4.85% | $0 | $0 | Yes ($250K) |

| Discover Online Savings | 4.80% | $0 | $0 | Yes ($250K) |

| American Express HYSA | 4.75% | $0 | $0 | Yes ($250K) |

💡 Key takeaway: Every top-rated high-yield savings account in 2026 charges zero monthly fees and requires no minimum opening deposit, removing all barriers to earning superior interest income.

🎯 How to Choose the Best High-Yield Savings Account in 2026

With dozens of high-yield savings accounts competing for your attention, it can feel overwhelming to pick the right one. But the decision becomes much simpler when you apply a consistent evaluation framework. The four factors that matter most are: the APY (Annual Percentage Yield), account fees, ease of access to your funds, and the platform's overall digital experience. Think of this process like hiring a financial tool — it should work hard for your money, stay out of your way, and be available when you need it. While a difference of 0.10% APY between two accounts may seem trivial, on a $50,000 balance it equates to an extra $50 per year in interest — not life-changing, but meaningful when compounded over time. Always read the fine print, because some accounts advertise a high headline rate but bury conditions like requiring a direct deposit of a specific amount to unlock it.

Beyond the numbers, consider the practical usability of each account. Can you link it to your primary checking account at another bank? How long do transfers take — one business day or three? Does the mobile app allow you to set up automatic savings transfers or create sub-accounts for different goals like a vacation fund, emergency fund, or home down payment? Banks like Ally Bank have popularized the concept of savings 'buckets' — essentially virtual sub-accounts within a single HYSA — which can be a powerful behavioral finance tool. SoFi takes things further by offering a combined checking and savings experience with features like early paycheck access and automatic APY boosts for members who set up qualifying direct deposits. The best account for you ultimately depends on your personal financial habits, how often you plan to access the funds, and which platform's ecosystem aligns with your broader banking relationships.

Compare APYs on a like-for-like basis

Before anything else, verify the actual APY — not the promotional or teaser rate — by checking the account's official disclosure page or a trusted aggregator like Bankrate, NerdWallet, or DepositAccounts.com. Some banks advertise a high rate that only applies to the first 90 days or requires conditions like a minimum direct deposit. The Annual Percentage Yield already accounts for compounding frequency, so it's the most accurate number to compare across accounts. As of 2026, look for accounts offering at least 4.75% APY as a baseline, with top performers exceeding 5.10%. Always bookmark the rate page and revisit it quarterly, since variable rates can shift with Federal Reserve policy announcements.

Verify FDIC or NCUA insurance coverage

Never deposit money into a savings account — high-yield or otherwise — without confirming it is FDIC-insured (for banks) or NCUA-insured (for credit unions). Both programs protect deposits up to $250,000 per depositor, per institution, per ownership category. Some fintechs like SoFi partner with multiple FDIC-member banks to offer pass-through insurance coverage up to $2 million, which is ideal for larger savers. You can verify any institution's insurance status instantly using the FDIC's BankFind Suite tool at fdic.gov. This single step eliminates the biggest risk associated with moving your money to an unfamiliar online bank and should always be your first due-diligence checkpoint.

Evaluate fees and minimum balance requirements

The best high-yield savings accounts in 2026 uniformly charge zero monthly maintenance fees and impose no minimum balance requirements to open or maintain the account. This wasn't always the case — legacy banks still charge $5 to $25 per month unless you maintain balances of $1,500 or more. Those fees can effectively eliminate the interest earnings advantage of a high-yield account entirely. Before committing, scan the fee schedule for potential charges like excessive withdrawal fees (some accounts still limit you to six free withdrawals per month under historical Regulation D guidelines, though the Fed suspended this rule in 2020, individual banks may still impose it), wire transfer fees, or paper statement fees. A truly fee-free account maximizes your net return without hidden deductions.

Test the transfer speed and digital experience

Your high-yield savings account should integrate seamlessly with your existing checking account, whether it's at a major bank, a credit union, or another online institution. Linking accounts is typically accomplished through a micro-deposit verification process or instant verification via services like Plaid, and most top banks complete this within one to three business days. Once linked, evaluate how quickly transfers move — same-day or next-business-day ACH transfers are now considered standard among premium providers. Download the mobile app and explore features like automatic savings rules, spending round-ups, goal-setting tools, and push notifications for balance changes. A polished, intuitive digital experience isn't just a convenience — it directly influences whether you'll develop strong savings habits over time, which is ultimately the whole point of opening a high-yield account in the first place.

⚖️ High-Yield Savings Accounts vs. Other Savings Vehicles: Pros & Cons

A high-yield savings account is an excellent tool, but it's not the only option for growing your cash reserves in 2026. Alternatives like Certificates of Deposit (CDs), Money Market Accounts (MMAs), Treasury bills, and I-Bonds each have distinct advantages and trade-offs. The core question is liquidity vs. yield: how quickly might you need access to your funds, and how much rate premium are you willing to forgo in exchange for that flexibility? HYSAs strike the best balance for most people — they offer competitive APYs above 4.75%, full FDIC insurance, and on-demand access to your money without penalty. CDs, by contrast, may offer slightly higher rates (some 12-month CDs are yielding above 5.30% in 2026) but lock your money away for a fixed term, charging early withdrawal penalties that can erase months of interest earnings if you need the cash unexpectedly. For most emergency funds and short-term savings goals, a high-yield savings account remains the optimal vehicle.

Treasury bills (T-bills) are another strong competitor in 2026, with 3-month and 6-month T-bills yielding between 5.00% and 5.40% at recent auctions. They offer the added benefit of being exempt from state and local income taxes, which is a meaningful advantage for residents of high-tax states like California or New York. However, T-bills require purchasing through TreasuryDirect.gov or a brokerage account, add a layer of complexity, and also lock up funds for the chosen term. Money Market Accounts (MMAs) from traditional banks often come with debit card and check-writing privileges, making them more accessible than a standard HYSA, but they frequently carry higher minimum balance requirements (sometimes $10,000 or more) and offer slightly lower APYs than the best online savings accounts. The smart approach for most savers is to use a HYSA as the core savings vehicle and supplement it with short-term CDs or T-bills for funds you know you won't need for 3–12 months, creating a simple cash laddering strategy that maximizes yield without sacrificing emergency liquidity.

Pros

- ✅ No lock-in period: Unlike CDs, HYSAs allow you to withdraw funds at any time without early withdrawal penalties, preserving full liquidity for emergencies.

- ✅ FDIC-insured safety: Your principal is 100% protected up to $250,000 per institution, making HYSAs among the safest interest-bearing vehicles available.

- ✅ Significantly higher yields: Top accounts in 2026 pay 10x or more than the national average savings APY, generating hundreds or thousands of dollars more in annual interest.

- ✅ Zero fees at top providers: The best high-yield savings accounts charge no monthly fees, no minimum balance fees, and no opening deposit requirements, maximizing your net return.

Cons

- ❌ Variable APY risk: Rates are not fixed — if the Federal Reserve cuts interest rates, your HYSA APY will likely decrease within weeks, potentially significantly reducing your earnings.

- ❌ No debit card or check writing: Most HYSAs are pure savings vehicles with no transactional features, requiring a separate checking account for day-to-day spending.

- ❌ Transfer delays: While many top banks now offer fast ACH transfers, moving large sums to your checking account may still take 1–2 business days, which can be inconvenient in urgent situations.

⚠️ Important tip: Always read the fine print on advertised APYs. Some banks require a qualifying direct deposit of $1,000–$5,000 per month to unlock their highest advertised rate. If you don't meet that condition, your actual APY may be significantly lower than the headline figure. Always confirm the rate you'll *personally* qualify for before opening an account.

✅ Maximizing Your Earnings: Smart Strategies for HYSA Users in 2026

Opening the best high-yield savings account is just the first step — how you use it determines how much wealth you actually build. One of the most powerful strategies is automating your savings contributions. Set up a recurring automatic transfer from your checking account to your HYSA every payday, even if it's just $50 or $100 per week. Because the money moves before you have a chance to spend it, you eliminate the friction that derails most manual savings efforts. Over 12 months, consistent $200 bi-weekly transfers into an account earning 5.00% APY will generate approximately $5,200 in new deposits plus roughly $130 in interest — a meaningful and growing emergency fund built almost effortlessly. Many platforms, including Ally Bank and SoFi, allow you to automate these transfers with a few taps in their mobile apps, and some even let you set savings goals with progress tracking to keep you motivated throughout the year. The behavioral aspect of saving is just as important as the mathematical one — automation addresses both.

Another strategy worth embracing in 2026 is rate monitoring and account switching. Because HYSA rates are variable, the account with the best rate today may not hold that title in six months. Bookmark a rate comparison tool like DepositAccounts.com or Bankrate and check it every quarter. If a competitor is offering a rate that is 0.50% or more higher than your current account, it may be worth the minor hassle of opening a new account and transferring funds. Most online banks complete the account-opening process in under 10 minutes, and many actively court transfers from competing institutions. Additionally, consider the tax implications of your HYSA earnings: interest income is taxable as ordinary income at the federal level and most state levels. For a saver in the 22% federal tax bracket earning $500 in annual HYSA interest, that's approximately $110 owed at tax time — factor this into your net yield calculation, and consider a tax-advantaged account like a Roth IRA or HSA for longer-term savings to complement your HYSA strategy. Diversifying your savings structure across these vehicles is what separates average savers from truly strategic ones.

❓ Frequently Asked Questions

✍️ Final Thoughts: Your Next Step Toward Smarter Savings

In 2026, there has never been a better time to be a disciplined saver with access to the best high-yield savings accounts on the market. Rates above 5% APY represent a generational opportunity — for most of the 2010s, top savings rates barely crept above 2%, and millions of Americans became accustomed to their money sitting idle earning almost nothing. That era is over. The difference between leaving $20,000 in a big-bank savings account at 0.45% APY and moving it to a top online HYSA at 5.10% APY is approximately $1,000 in additional interest income per year — real money that compounds further every year you stay invested in a high-yield account. The top accounts we've covered — SoFi, Marcus by Goldman Sachs, Ally Bank, Discover, and American Express — all share the same winning formula: zero fees, no minimum balance requirements, full FDIC insurance, and competitive rates backed by reputable institutions. Choosing among them comes down to which platform's features, mobile experience, and transfer ecosystem best fits your personal financial life. The most important thing is simply to make the move — every month you delay is another month of potential earnings lost forever.

Here is exactly what you should do right now: First, identify your current savings account APY — log in to your bank's app or website and look up your account's interest rate. If it's below 3.00%, you are almost certainly leaving money behind. Second, pick one account from our top five list and open it today — the process takes under 10 minutes for most online banks, and you need only a government-issued ID and your existing bank's routing and account numbers. Third, set up an automatic recurring transfer from your checking account to your new HYSA — even $100 per month builds the habit and compounds meaningfully over time. Fourth, put a quarterly calendar reminder to re-check rates, especially around FOMC meeting dates, so you can respond quickly if the rate landscape shifts. Financial freedom doesn't come from a single dramatic decision — it comes from consistently making small, smart choices that compound over months and years. Opening the right high-yield savings account today is one of those choices. Your future self — with a healthier emergency fund, a growing down payment, or simply more financial breathing room — will thank you for acting now rather than later. Visit InfoWellHub.com for regularly updated rate comparisons, expert financial guides, and the tools you need to make every dollar work as hard as possible in 2026 and beyond.

Post a Comment